In connection with the anticipated opening of a new Essex County Jail in Lewis, N.Y., during the summer of 2007, the New York Correction History Society (NYCHS) created this "virtual tour" of pre-computer record keeping at Essex County's old jail in Elizabethtown.

The tour begins with an examination of the "Cash Book," one of three jail ledgers made available to NYCHS for this purpose by Major Richard Cutting, Essex County Jail Administrator since 1977.

In that ledger were recorded the Essex County Jail Inmate Accounts covering April 2, 1952 to March 18, 1958.

Since the grand opening of the jail in Lewis was scheduled for the summer of 2007, the NYCHS webmaster decided to focus examination on the inmate Cash Book transactions of a half century earlier -- Anno Domini 1957.

The "Cash Book," measuring 12 by 7 1/2 inches, features an alphabetized group of 30 pages at the front, followed by 272 numbered pages.

Upon admission, an inmate's folding money and coins -- assuming he or she had any -- were confiscated and their amount became the opening balance of the account started in the Cash Book for that inmate on the first available numbered page. That page's number would be entered with the inmate's name on the first available line on a lettered page matching the initial letter of his or her last name.

The numbered pages provided a record of inmates' own monies held during their incarcerations -- the starting amount, the individual transactions, and a running tally of the balances. The lettered pages at the front of the ledger served as an index for finding the numbered page(s) for a particular inmate.

The bookkeeping process would usually begin at in-take when the inmate's name was entered in one of the 30 alphabetized pages in the front of the book, depending upon the first letter of his or her last name.

On the same line would be entered the numbered page of the initial entry for that inmate's account.

The inmate, family members, or friends could add to the balance by depositing cash or checks to be credited to the account. Upon discharge, the inmate received the remaining balance.

This web presentation begins with the Cash Book's first full page filled with 1957 entries.

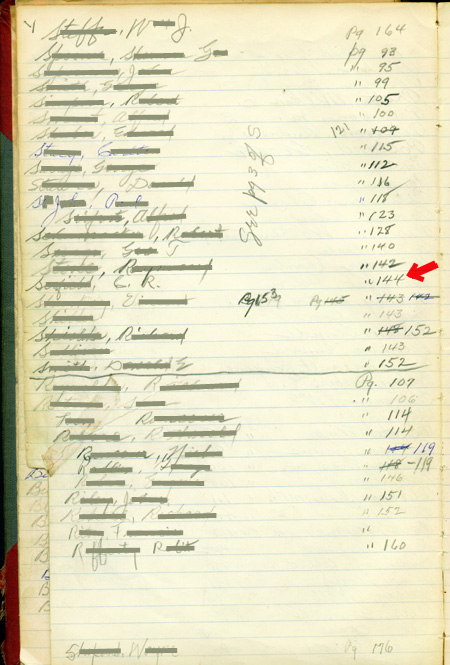

They happen to have been generated beginning Jan. 21, 1957 by an inmate with the initials C. R. S.

His name became the 16th entry on one of the two pages reserved for inmates whose last names began with the letter "S" or the letter "R." (See page image below left.)

Click image for full 450-point wide version, as per "Expand Images" box instructions right. Use back button to return to this page. Click image for full 450-point wide version, as per "Expand Images" box instructions right. Use back button to return to this page. |

Across from his name was listed the number of the page where his account was begun -- Page 144.

EXPAND IMAGESBeginning left, the next 8 ledger images are reduced versions of 450-point wide JPGs. Click the reduced version on this page to have your browser bring up the full 450-point wide JPG. Use your browser's expand image icon  (example right: IE expand image icon)

to expand that JPG to its full width. Use the browser's "back" button to return to this page. (example right: IE expand image icon)

to expand that JPG to its full width. Use the browser's "back" button to return to this page.

|

|

In this presentation, only inmate initials are shown. On the scanned images of the pages (not on the actual pages) the other letters in inmate names have been "crossed out" digitally by the NYCHS webmaster.

That is because this part of the ledgers presentation seeks to show how pre-computer record keeping was done at the old jail. It is not intended to identify any inmates.

Indeed, the actual pages of the Cash Book provide no inmate identification beyond names -- no ID numbers, ages, dates of birth, addresses, heights, weights, eye and hair color, or other identification data.

In a jail with a maximum capacity of perhaps two dozen inmates, an inmate's name was enough for Cash Book purposes.

Click image for full 450-point wide version, as per "Expand Images" box instructions above. Use back button to return to this page. Click image for full 450-point wide version, as per "Expand Images" box instructions above. Use back button to return to this page. |

Also digitally added to the images in this presentation are red arrows pointing to particular details mentioned..

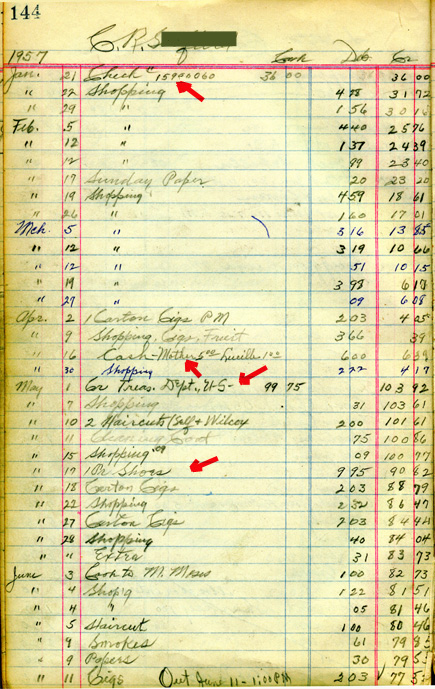

On Page 144 -- as on all the numbered pages -- columns provided space for entering dates of transactions, the beginning cash balances, brief notes on transactions, each debit, each credit and the running balance.

The cash record for C. R. S. on Page 144 began Jan. 21, 1957 with $36 from a check #15940060. That would suggest that perhaps he had no folding money on him at the very start of his incarceration and that his account began sometime later with the cashing of the check.

On May 1st he cashed a $99.75 federal government check (Social Security?).

During his approximately five-month stay, he spent $58.23 on such items as haircuts ($1 each), cigarettes ($2.03 a carton), and newspapers.

C. R. S. on April 16th gave his mother $5 from his jail account and $1 to someone named "Lucille."

On at least one occasion he paid for a fellow inmate's haircut and on another occasion he gave a different inmate $1 from his jail funds (perhaps for a haircut).

Click image for full 450-point wide version, as per "Expand Images" box instructions above. Use back button to return to this page. Click image for full 450-point wide version, as per "Expand Images" box instructions above. Use back button to return to this page. |

One interesting item he purchased while an inmate was a pair of shoes -- for $9.95 on May 17th. When discharged from the jail June 11, he took with him his remaining balance of $77.52 and, presumably, his new shoes on his feet as he walked out the door.

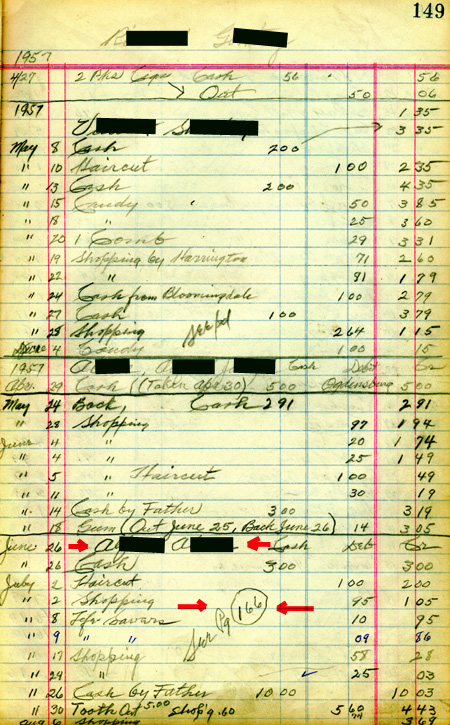

Not all inmate accounts began and ended on the same page as did the cash record for C. S. R.

More often than not an inmate account began on a page shared with other accounts and would be continued on one or more subsequent pages.

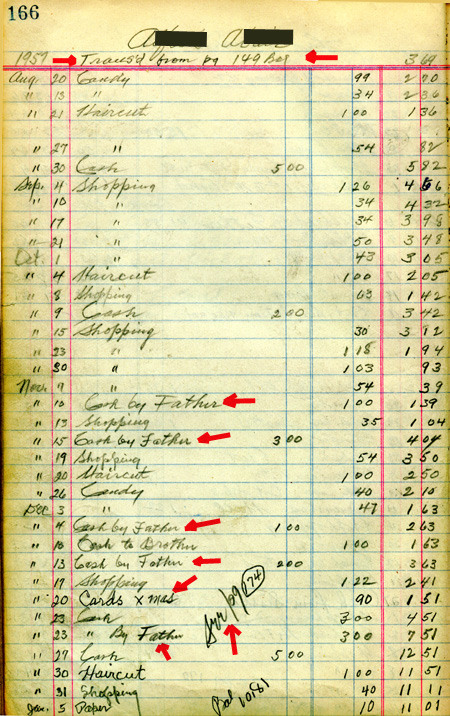

For example, the account for inmate A.A. began June 26 near the bottom of Page 149 (including 10 cents for a pack of Life Savers on July 8th and $5 for a tooth extraction July 30) and was continued Aug. 30 on Page 166, from which it continued Jan. 7 onto Page 174 with 1958 entries until his discharge on Feb.21.

When a record "jumped" to another page, a notation would be entered -- such as "See Pg. 166" -- giving the number of the page on which the continuation could be found. Where the continuation began, a notation would be entered -- such as "balance transferred from Pg. 149" -- giving the number of the page from which the inmate account record was being continued.

Click image for full 450-point wide version, as per "Expand Images" box instructions above. Use back button to return to this page. Click image for full 450-point wide version, as per "Expand Images" box instructions above. Use back button to return to this page. |

One of the more interesting aspects of the A. A. entries on Pages 149 and 166 is the frequency with which his father kept adding modest amounts of cash to the son's account: $10, $1, $3, and $2 at various times,

Most expenditures recorded with particulars on Pages 149, 166 and 174 went to candy, haircuts, "cigs" and newspapers, but on Dec. 20 A. A. did spend 90 centes for "Xmas Cards."

Nineteen expeniture entries -- individual amounts ranging from 25 cents to $1.26 -- carried the very vague generalization "shopping."

What that term entailed is unclear but among all entries in the Cash Book, it was the most frequently used notation.

One theory is that the term was used to cover several different items purchased the same day, whereas if only one item was purchased on the given day, only that one would be recorded.

But that multiple-item theory appears weakest when attempting to explain use of the notation to cover expenditures as low as 25 cents in A. A.'s account and even lower in other inmate accounts.

Click image for full 450-point wide version, as per "Expand Images" box instructions above. Use back button to return to this page. Click image for full 450-point wide version, as per "Expand Images" box instructions above. Use back button to return to this page. |

Nevertheless, prices in 1957 were indeed sufficiently low that one daily newspaper, one pack of gum and one candy bar might cost a total of 25 cents.

So, perhaps some Cash Book keepers elected to write "shopping" to cover all those things rather than itemize.

If anyone reading this has a better grasp of what "shopping" meant in the Essex County Cash Book inmate account context, please let the webmaster know. He would add the information to this web page.

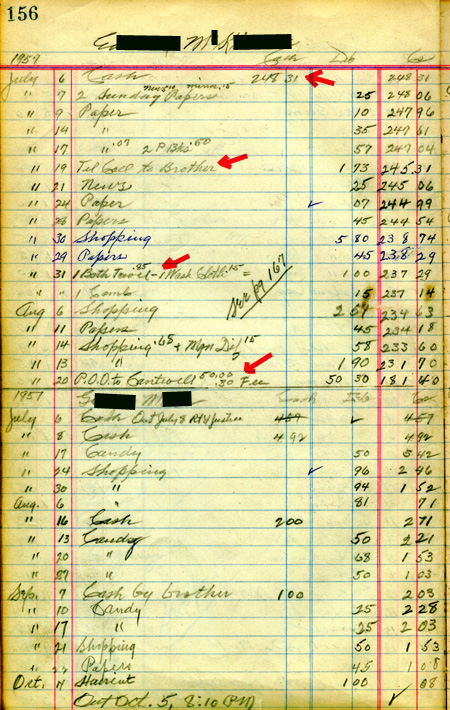

Another example of an inmate account opening on one numbered page and, after some entries, continuing onto another numebered page is that of E. M. K.

His account record began June 6 on Page 156 with a start-up of $248.31, the largest single opening balance credited to any inmate in 1957.

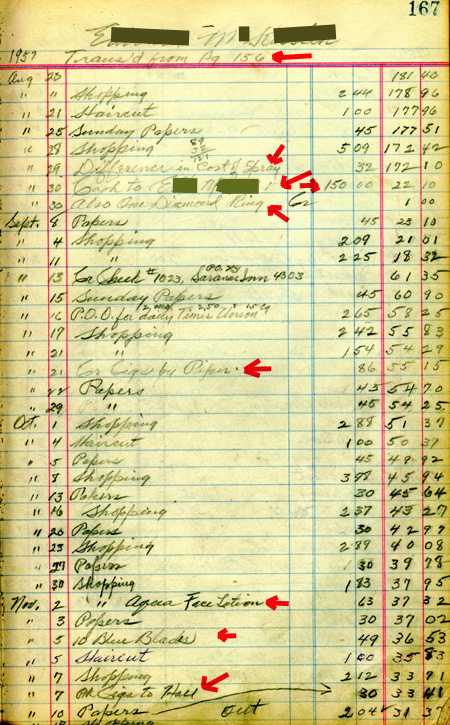

His account conitinued on Page 167, with entries filling the entire page. Rather than continue the account onto yet another page, his discharge was "squeezed in" at the bottom with insertion of the word "Out" floating in vicinity of the last purchase entry on Nov. 13: $2.04 worth of shopping. His final balance was $31.37, considerably more than what most inmate accounts began with as their opening balance.

Click image for full 450-point wide version, as per "Expand Images" box instructions above. Use back button to return to this page. Click image for full 450-point wide version, as per "Expand Images" box instructions above. Use back button to return to this page. |

The list of his expenditures contrasts markedly with the items usually purchased by other inmates. He bought no candy. He didn't buy cigarettes for himself but paid cigarette purchases on behalf of other inmates -- for Piper on Sept. 21 and for Hall on Nov. 7.

E. M. K. appears to have been an avid reader. Newspapers constituted the leading item listed: 21 separate entries. Indeed, the fifth entry line in his opening Cash Book record page 156 includes two pocketsize books ("2 P Bks" for 50 cents on July 17th).

After reading material, the next leading category of itemized entries was grooming/hygiene: an 81 cents bath towel, a 15 cents wash cloth, and a 15 cents comb, all on July 31st; (hair?) spray on August 29th, 63 cents Acqua Face Lotion on Nov. 2nd, 49 cents 10 Blue Blades (shaving) on Nov. 5th, and three haircuts, a dollar each.

On July 19th E. M. K. spent $1.79 phoning his brother ("Tel Call to Brother"). The inmate sent a $50 postal money order to someone named "Cantwell," perhaps an attorney, on Aug. 20. Ten days later he sent $150 and a diamond ring to a woman with the initials E. M.

If imagination were allowed free reign, what melodramatic stories of ill-fated romance could be woven and embellished from those scant Cash Book entries.

Click image for full 450-point wide version, as per "Expand Images" box instructions above. Use back button to return to this page. Click image for full 450-point wide version, as per "Expand Images" box instructions above. Use back button to return to this page. |

For some unknown reason, this particular Cash Book's inmate account entries end in March 1958 on Page 179, leaving the ledger's lines and columns blank on the remaining approximately 90 numbered pages.

Did a new system of record keeping begin? Or new jail administration wanting to start with a set of fresh ledgers of its own, including a new Cash Book? Anyone with information shedding light on the question, let the webmaster know so he can add that to this web page.

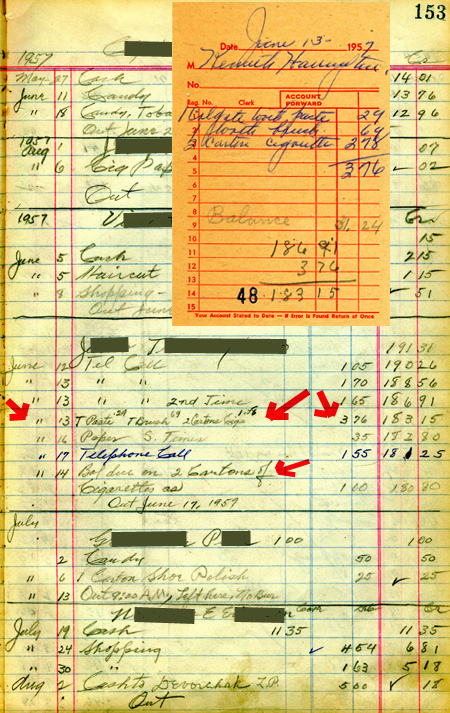

Tucked between two of the 90 pages without entries was a 5 inch by 3 1/2 inch sales receipt (see insert image left) made out, in blue ink or carbon paper blue color, to a Kenneth Harrington (?) on June 13, 1957 for 1 Colgate tooth paste (29 cents), 1 tooth brush (69 cents), and 2 cartons of cigarettes ($2.78) for a total of $3.76.

The transaction seems to have involved a $5 bill because the sales slip includes the notation, apparently in pencil and different handwriting, "Balance $1.24." A third set of notations in darker pencil subtracts the $3.76 from $186.91 for a remainder of $183.15.

A quick review of the 1957 inmate account pages finds on the ledger book's Page 153 a June 13th entry for an inmate with the initials J. T. for "T Paste .29, T Brush .69, 2 Cartons Cigs 1.78." The $1 difference between the $2.78 cost of the 2 "cigs" cartons on the sales slip and the $1.78 entry in the account book is adjusted in the last entry at the time of his release July 17th but is backdated to June 14th. Perhaps that backdated adjustment is why the sales slip with the original correct amount was tucked away in the back of the book, just in case any question arose about the bookkeeping correction.

Click image for full 450-point wide version, as per "Expand Images" box instructions above. Use back button to return to this page. Click image for full 450-point wide version, as per "Expand Images" box instructions above. Use back button to return to this page. |

Inmate J. T. stayed only five days during which his most frequent expenditures were phone calls: one on June 12th to begin the account, two on June 13th, and a fourth on June 17th, the day of his discharge. The account began with an initial balance of $191.31 and closed with a final balance of $180.80.

The "Kenneth Harrington" named on the sales slip was probably a jail staffer. That tentative conclusion is based on the fact that the receipt was made out to him, rather than to inmate J. T.

It is also more likely that a staffer, not the inmate, made the sale slip calculations subtracting the items' total cost from the Cash Account's previous running balance.

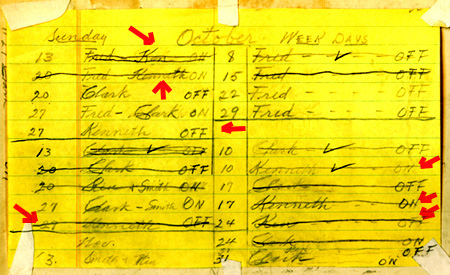

An additional factor favoring "Kenneth Harrington" having been a jail staffer is a section of lined yellow paper taped on the inside of the ledger's back cover.It appears to have been jail work schedule for Kenneth and/or Ken, Fred, Clark and Smith, perhaps of a staffer schedule for Cash Book responsibility.

It's not clear whether "Kenneth" and "Ken" on the schedule were one and the same person or two people with the same first name, one of whom was called Ken to distinguish him from the other called Kenneth.

This webmaster leans to the one-person theory because use of last names would ordinarily have been an easier and less confusing way to write up a work schedule involving two people with the same first name. Was "Smith" a first or last name? "Clark" could be either a first or last name.

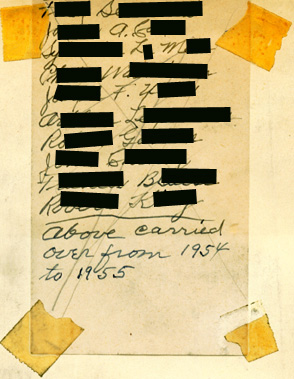

On the totally blank unnumbered page facing the inside of the ledger's back cover was a taped note with 10 names of inmates.

It was captioned "Above carried over from 1954 to 1955."

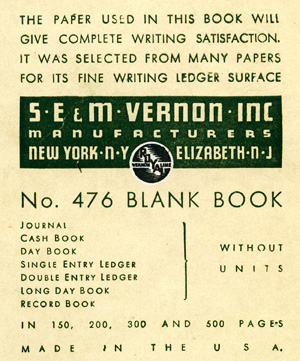

On the inside of the front cover was a label of its manufacturer, S. E. & M. Vernon Inc., of New York, New York and Elizabeth, N.Y. featuring the Royal Writing watermark.Research indicates the company, once based at 65 Duane St., NYC, went out of business in the 1960s.

What this little "virtual tour" of the 1952/58 Cash Book makes clear is that ledger book entries with careful note-taking enabled Essex County jail staffers a half century ago to keep track of inmate accounts, without barcodes and computers. The prices seem shockingly low by 2007 standards. Cigarettes, banned in many jails today, were a major purchase item back then. Phone calls and candy constituted major inmate expenditures then as now. Today many jails make newspapers available without charge in the common day room areas. Toiletries remain items much in demand.

While inmate account record keeping methods and the pattern of inmate purchases may have changed from era to era, the need for keeping such records has remained a constant so far.

-- NYCHS webmaster